PHOTO: ST FILE

Updated from : The Business Times, 19 Jan 2021

A FEARED slump in the private property market did not quite materialise in 2020; and with the ongoing momentum in the sales of private homes, things may have turned a corner for developers heading into 2021.

Despite the pandemic, the Private Residential Property Index rose 2.2 per cent for 2020 as a whole after notching a quarter-on-quarter gain of 2.1 per cent in Q4 2020, based on the Urban Redevelopment Authority’s (URA) latest flash estimate.

This came even as the pandemic sent the economy spiralling into a recession, with gross domestic product (GDP) contracting 5.8 per cent last year, advance estimates from the Ministry of Trade and Industry showed.

The surprising climb in private home prices likely arose from a confluence of factors. Among them are the slew of measures announced by the government last year to combat the pandemic – including the deferment of mortgage payments and the introduction of wage subsidies – which helped to save jobs and indirectly supported the property market.

At the same time, the pandemic has affected industries differently – with those such as travel almost paralysed by border closures and the “circuit breaker” in Q2.

Others – such as the information and communications, finance and insurance as well as professional services sectors – fared better and posted an expansion.

Higher-income earners and/or those with robust household balance sheets may have chosen to plough funds in the property market – which has proven less volatile than the stock market – while demand from Housing Development Board (HDB) flat upgraders as well as low mortgage rates also served to bolster the market, analysts said.

With the vaccine roll-out underway in Singapore and the economy poised to recover gradually, the outlook for developers appears more positive in 2021 than it did previously.

The low interest rate environment could also give prospective home buyers the impetus to take the plunge, while an eventual lifting of border control measures this year would likely act as a shot in the arm for sales of luxury projects, as travel restrictions largely kept foreign buyers at bay last year.

In 2020, it was the demand for mid-tier and mass market projects which helped to nudge private home prices upwards.

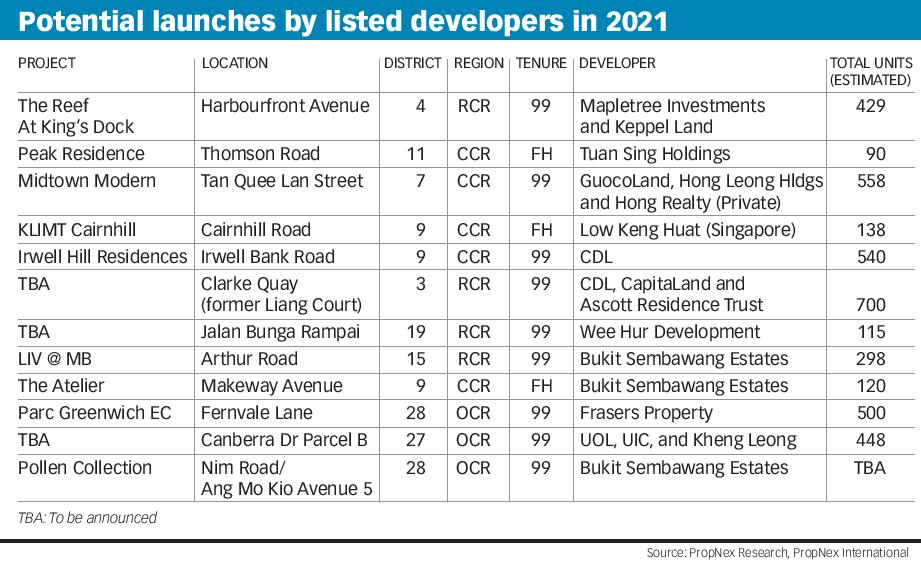

There has also been talk of the en bloc market – dampened by the last round of cooling measures in July 2018 – picking up again in 2021 as developers look to replenish their landbank. Small to medium sites of up to 500 units are likely to be on developers’ radar given the relatively lower development risks, said Huttons Asia. This comes as the inventory of unsold units has continued to decline on the back of firm demand, while supply under the Government Land Sales programme remains moderate.

Though the road to recovery could see some hiccups along the way, OCBC Investment Research remains overweight on Singapore-listed developers such as CapitaLand (fair value: S$3.75), UOL (fair value: S$8.48) and City Developments (fair value: S$9.65) on the back of attractive valuations as investors continue the rotation into value and cyclical sectors.

RHB analyst Vijay Natarajan, who expects private property prices to rise as much as 3 per cent this year, reckoned the ongoing momentum in new home sales will serve as an earnings catalyst, with new home sales volumes possibly clocking 9,000 to 10,000 units.

“Most developers also have a high proportion of recurring income streams from investment properties, which should see a rebound on the back of an absence of rent rebates and an overall pick-up in the economy,” he said in a research note, ruling out further write-downs or impairments to capital values for now.

To be sure, risks remain, with analysts flagging potential downside risks such as the abrupt tapering off of government support measures, the softer rental market, a rise in unemployment as well as the possibility of the government introducing fresh cooling measures to curb runaway prices. A flare-up in the number of Covid-19 cases could also affect property sales in the near term.

The resilience displayed by the property market thus far, however, suggests that developers have cause to be – at least – cautiously optimistic in 2021.

You must be logged in to post a comment.